Category Archives: economics

Iran, the Straits, and the Looming Crisis for the West

A truly alarming situation is developing for the G20 advanced economies. If not handled deftly, its outcome threatens more disastrous consequences for those economies than the events following the oil crisis of the early 1970s. One of the world’s four choke points carrying 20% of its oil and gas has been shut down, and another could easily follow. Nothing like this has ever happened before.

If the religious fanatics of Iran ask their Houthi proxies in Yemen to up the tempo of their strikes in the approaches to the Suez Canal, Europe will shut down. Reserves will be exhausted in a matter of weeks — days in some cases like ours.

How, you might ask, do the mad mullahs have the power to achieve this? The Houthi insurgents of Yemen look to them for their supply of weapons, and both share a visceral hatred of Israel. Altogether, it would represent a doomsday scenario for the embattled democracies.

In such a situation, the gloves would have to come off. Any pretence at playing Mr Nice Guy would end, and the democracies, east as well as west, would feel obliged to offer their military assets to re-open these choke points to save their economies from collapse. It might well be that military occupations of the zones for a period of time would be judged necessary.

It might also be decided for future stability that if boots have to be put on the ground, the opportunity should be seized to rid the world once and for all of the theocratic regime that has brought such murder and disruption to the world. Certainly, the toppling of the regime would be welcomed by a very large majority of the population, its entire sisterhood for a start. As a result, regime change would be unlikely to be a protracted affair.

Sadly, and depressingly for future generations, recent events in Iran have demonstrated that street uprisings can no longer bring down a tyranny if that tyranny is ruthless enough to murder enough people. And that is what the ‘Holy Men’ of Iran were prepared to do — tens of thousands in this case. Only if the men with guns turn against the mullahs can change occur internally. For the moment, the promptly and well-paid 125,000 men of the Revolutionary Guard are, and are prepared to remain, loyal to their master’s dirty work.

As in Afghanistan, and sadly throughout the Muslim world, a high proportion of men quite like their faith’s legitimising male power over women. This explains why the Iranian authorities are able to mount counter-demonstrations. Look for the women among the demonstrators, and you’ll be pushed to find them. But before we get on our high horse, we should remember that our own societies were highly patriarchal only a few generations ago, though this was not mandated by scripture as it is in Islam.

With the USA and Israeli air and naval assault on Iran to neutralise its nuclear and rocketry ambitions, the aims have widened to regime change. But history has taught us that no amount of damage from the air, short of nuclear strikes, can achieve that end. Iranian cities bear no resemblance to those of Hitler’s or our own, come to that. But even so, neither of us considered surrender.

It is a great deal easier to get into things than to get out. If boots on the ground are forced on the West to secure free passage through the straits, then to quote Macbeth, ‘If it were done when ’tis done, then ’twere well it were done quickly.’ And in this case, with such majority hatred of the clerical killers of their sons and daughters, I believe it would be quick. Iranians are a clever and gifted people. There is no reason to believe that if the ghastly, evil regime that has held them in thrall for almost half a century is cast into the dustbin of history, they will not be capable of becoming a normal country and ruling themselves competently. Their civilisation, after all, was once a beacon to the world, tolerant and much admired by Alexander the Great.

The loss of the West’s confidence began with Vietnam. It continued through the fiascos of Afghanistan, Iraq, Libya and Syria. In earlier times there had been triumphs such as the Berlin Airlift, the forming of NATO, the Cuban missile crisis, and the landing on the moon. Going into countries with all guns blazing proved to be the easy bit, but putting together an exit strategy proved altogether harder. Part of the problem was a lack of understanding of the complexities of the regions they were operating in. The Middle East and Muslim world, with its Shia-Sunni divide, was made even more complex by the colonial powers’ ill-thought-out settlement of frontiers following the destruction of the Ottoman Empire. It enabled an entirely new state, Israel, to be set up, creating the thorniest issue of the lot.

Into this china shop has stormed the proverbial bull in the form of the American president. Ironically, Trump’s very unpredictability can sometimes achieve results that plodding diplomacy struggles to keep up with. If the degrading of the bestial regime in Tehran can bring about its collapse, the world and most of all Iranians should rejoice. There is everything to play for, and with luck the world’s most troublesome area may have a chance to settle down, with its remaining tyrants sleeping less easy in their beds.

CANZUK: A Marriage Made in Heaven

There are few political outcomes about which any of us can be certain. However, the coming together of the Anglosphere seems almost assured. I am certain that when it happens, it will be a great boost for liberal democracy, becoming at a stroke the third pillar of the Free World after the US and the EU. It will also, at one leap, become one of the largest economic and military entities on the planet.

I speak, of course, of the settler communities of Canada, Australia, and New Zealand reuniting with their founder. A bipartisan poll has shown massive support in all four countries. While keeping their own parliaments, they propose to operate in unison in such areas as freedom of movement, job opportunities, recognition of each other’s qualifications, free trade, common currency; defence and intelligence, along with a joint defence policy. All will enjoy a high level of autonomy, much like the four countries of the UK.

This profound development could not have happened before this time. But a growing chorus argues that its time has come. Each of the now established nations needed to break free from the coattails of their founder, mature in their own right, shaking off any feelings of inferiority to their ancient motherland, and establish their own identity. This, over long years of autonomy, they have successfully achieved. All three punch well above their weight and are a credit to both themselves and their founder. The same could be said of the mighty United States, though its weight can never be in doubt.

Although the four nations of the proposed new union have been free for well over a hundred years to set their own policies, they have remained in remarkable lockstep with each other. So much so that if any of their citizens were to uproot themselves to another of the quartet, they would not feel themselves to be in a foreign land. So similar are all their institutions and the way they go about their daily lives, and so similar are the things they hold dear, that it is not surprising that such massive majorities for a reunion were achieved.

However, the world in which all four now operate has changed beyond all recognition. Who could have imagined that backward, dirt-poor China that occupied Australia’s backyard when it gained its independence would now be a digital, financial, and military colossus that casts a menacing shadow over its empty spaces, rich with rare earth materials and everything you can think of? How could Canada have known, when it achieved its independence 158 years ago, that its kindred neighbour to the south would grow so big as to make any dealings with it, trade or otherwise, totally unequal? Dangers and challenges surround these fledgling nations, as indeed they do their own mother-country since it left the EU. It is glaringly apparent that only their combined muscle can provide an answer.

Quietly and without fanfare, as is their preferred method, the nations of the Anglosphere are already reuniting. Britain’s exit from the EU has now got us back to where we were before that fateful sign-up decision that so upset our natural family. It has no option but to fashion a new future. In truth, it was never a proper fit with the EU, the successors of Charlemagne, wonderful as the concept of the EU was and is. It only joined because it was economically weak, while at the same time, Europe appeared prosperous. Britain’s horizons have always been global, notably marked by its history with the thirteen colonies. But that particular colossus, although it truly belongs in the proposed new union, cannot ever be a part. Ex-officio, maybe, but never a part. It is just too damned big. It couldn’t help itself from bossing the others around. Nevertheless, the emergence of a mighty new ally, fashioned in so many ways in its own image, could only but bring a smile to its face. The US would feel immense relief at no longer having to bear the burden of maintaining the post-war settlement alone. The creation of CANZUK (an acronym for Canada, Australia, New Zealand, and the UK) would also be a boost to the Commonwealth, various members of which, with closely aligned values, might well aspire to join. Singapore springs to mind, as it already shares a great many of these and is an economic fit.

Few would argue that the world would not be a better, happier, and more secure place, were CANZUK to become a reality. As we move into the New Year, I am hopeful that 2025 will see some truly positive developments, even if CANZUK is not one of them. 53 years of Syrian misery is at an end, and I believe that the present leadership means what it says about a Syria for all factions. Ukraine, too, I believe, will see an end to the war, though it cannot be that Putin can claim any sort of a victory. Also, I am sure that there will be a resumption of the Abraham Accords, once the guns fall silent in Palestine. Peace may, at last, come to that benighted region, which we — I am sorry to say, as the arbiters of the time — messed up on and which our progenitor nation, the US, will, hopefully, after a hundred years, make good on.

With all these things in mind, and many more, I would like to wish my own small family of readers a very happy and contented New Year.

Brexit and Beyond: Uniting the Old Commonwealth

On the seventh anniversary of Brexit, it is both disheartening and exasperating that the project remains shrouded in negativity, with scant attention paid to the opportunities it presents. A dazzling prospect lies in wait for the British government. By overwhelming majorities, the citizens of our erstwhile Commonwealth allies – Canada, Australia, and New Zealand – have signalled their wish for a revival of the kinship that united us at the dawn of the 20th century.

While steadfastly maintaining their sovereign parliaments, these nations envision sharing with us a common defence, security, and foreign policy. They also aspire to enable freedom of movement, commerce, recognition of qualifications, and much more. This collective interest embodies a potential union that could function exceptionally well. Our levels of employment and standard of living are broadly comparable, and almost all aspects of our societal framework; our values, culture, history, parliamentary system, law and language, are remarkably similar. If realised, this would form the largest union globally, and provide a sturdy pillar of support to a beleaguered Uncle Sam.

Objectively, such an endeavour could be considered a straightforward decision and one that should draw cross-party backing. So, why does Westminster hesitate to seize this momentous opportunity? Could Brexit yield a more significant dividend than to reunite our familial ties in such a monumental development? The renewal of this close relationship, now known as CANZUK, holds a promising future.

The emerging power of the CANZUK union

Democracy and our Western way of life are currently in crisis. The rise of a militarised China, a crazed and delinquent Russia, and increasing numbers of authoritarian states pose what some see as an existential threat to our Western values. Yet, a powerful development could potentially reverse this situation.

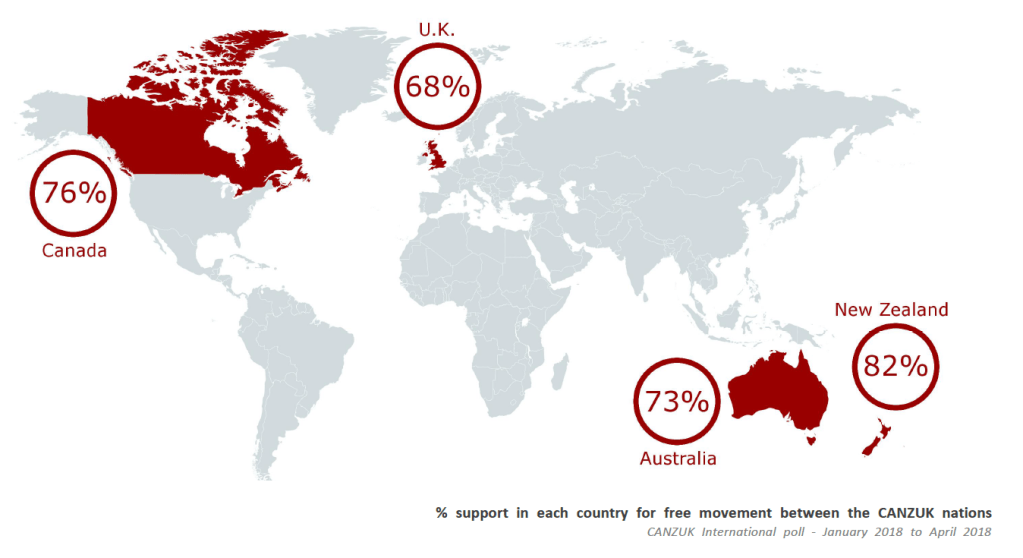

Forces are gathering for a union of four pivotal democracies – an entity known as CANZUK, an acronym for Canada, Australia, New Zealand, and the UK. Public polling indicates broad support: 68% in Britain, 73% in Australia, 76% in Canada, and 82% in New Zealand. Each nation will remain sovereign, yet they’ll cooperate in foreign policy, defence, freedom of movement and trade, recognition of qualifications, and sharing of security concerns—an existing example of such cooperation being the Five Eyes Agreement, which also includes the United States.

In terms of land area, this proposed union would be larger than Russia, boasting a combined GDP of $6.5 trillion and a population of 135 million. Its military budget would exceed $100 billion, making it the third largest in the world.

While many draw parallels between CANZUK and the EU, crucial differences exist. The CANZUK nations share a common language, heritage, and lifestyle. Their standard of living, employment levels, and political institutions run in parallel. Critics of CANZUK have termed it ‘a white man’s club’, but CANZUK International, the organisation advocating for the union, has stressed that the door will remain open to other like-minded nations sharing the same values, including India.

Historically, the CANZUK countries have fought together in defence of freedom, never against each other – unlike the turbulent history of European nations. Another critical difference with the EU is that no CANZUK nation will impose rules and regulations on another, unlike the centralised control from Brussels.

The emergence of the CANZUK union could reinvigorate global leadership, inspire the United States to remain globally engaged, and establish a third significant pillar of Western values alongside the US and EU.

Each CANZUK nation will also gain unique benefits. Canada could negotiate on more equal terms without the overshadowing presence of its giant neighbour. Australia and New Zealand could face China’s assertiveness more confidently, and Britain, once history’s largest empire, would regain its international influence and join the largest confederation on the planet – a reinvigoration sparked by Brexit during its dire straits.

The prosperity of CANZUK members could significantly increase as a result of this union. Critics who question the viability of trade due to geographical distances overlook the success of global trading giants like China and Japan. Advancements in AI and green technology, like the US Navy’s move towards virtually crewless ships, are likely to reduce shipping costs in the future, making the trading prospects even more favourable.

But perhaps the greatest beneficiaries of this promising development will be the young. They would be free to live, travel, study, and work across the expansive regions of CANZUK. Even retirees could benefit from the freedom to relocate. This exciting prospect is, to borrow a popular phrase, ‘a no-brainer.’ It should be for us grown-ups too.

The rise of the CANZUK union could potentially reinvigorate global leadership, inspire the United States to remain globally engaged, and establish a third significant pillar of Western values alongside the US and EU.

While Brexit initially represented a step away from supranational involvement for Britain, it may have ultimately set the stage for a stronger, more aligned union with countries that share deep historical and cultural ties. The post-Brexit era for Britain may not be one of isolation, but of renewed global influence and connectivity.

Many didn’t think Britain had much of a future outside the EU, but the world has always been our oyster. The CANZUK proposal is just one way we’re demonstrating that. Even domestically, we may find a solution to the aspirations of our member nations of the UK. As federal states within the union, they too could at last stand proud as sovereign states.

The notion of poor, tortured Ireland reuniting and choosing to join this new brotherhood of nations is not beyond the realms of possibility. This would be a testament to the appeal and potential of CANZUK, its promise of mutual benefit, and its respect for national sovereignty.

This is not a mere dream; it’s a potential reality within our grasp. It’s time to seize the opportunity and make CANZUK a part of our shared destiny. In an era marked by uncertainty and rapid change, the promise of CANZUK is a beacon of stability and shared prosperity, a testament to what nations can achieve when they unite under common values and a shared vision. Let’s look towards this future with hope and determination.

Schäuble needs a history lesson

Poor, benighted Greece. Yes, it lived beyond its means, encouraged by greedy bankers all too willing to see it mortgage its future. And, yes, the Greek way of doing things seems decidedly un-Germanic.

What an unedifying carry-on that scrambled, weekend marathon was, called to decide Greece’s fate and preserve the integrity of the euro. A two days’ notice summons went out to the nine heads of government not in the euro who were told to attend that Sunday. Then they were told to stand down. They didn’t need a grand council of all twenty-eight EU members after all. Talk about an omnishambles and the Grand Old Duke of York.

It was always meant to be that, once enrolled, you were as locked in as all fifty states of the American union are to the dollar. But it turns out that that this is not the case. Former Foreign Secretary William Hague once made the mistake of saying that belonging to the euro was like being in a burning building in which all the exit doors are locked. Really! Wolfgang Schäuble, the hard-line German finance minister, had actually drawn up a plan to show Greece the exit door if it did not comply with EU terms.

There are many truths to this latter day Greek tragedy. Ironic it is that it should happen to Greece of all countries, which wrote the scripts of the very first tragedies concerning the foibles of human nature. Just as it was beginning to make progress under austerity – though there remained much to do, as the latest Brussels proposals made clear – a crazy, economically illiterate cabal of schoolboy lefties gained power. (They once believed that Communism was the answer.) Their silly promises of an end to austerity were seized on by a weary electorate. But how could they work that particular piece of economic sophistry? It was like asking someone to turn base metal into gold.

We are today in a situation in which a mere eleven million Greeks labour under a mountain of debt equal to what our sixty-four million people spend on the NHS in a year and a half. It was, and is, insupportable.

Once again the banks have a case to answer. It is a truism that a lender has as much of a responsibility as the borrower. What is abundantly clear is that the lenders did not exercise due diligence. They knew the Greek character and that once they enjoyed the security of the euro with its low borrowing costs would, likely as not, go on a spending spree and end up living high on the hog, enjoying a standard of living way beyond what their productivity justified.

But while the good times rolled the banks looked the other way and that fatally flawed conception – a currency (monetary) union without a fiscal and banking one was able to bumble along… just. But it was never going to avoid the attention of the speculators on the world’s money markets when the good times ended, as they always do. And boy, did they end! When the banks were exposed as having lent to millions of mainly Americans (but, yes, us too) on mortgages that they knew were likely to go belly-up, they then artfully – and I believe criminally – wrapped up those toxic, sub-prime debts in packages mixed in with sound debts and unloaded them to unsuspecting other banks all around the world. The consequence was that every bank viewed every other bank with suspicion and would not lend to them (an absolutely necessary requirement under the capitalist system) for fear that the other bank had saddled itself with lashings of toxic debt and may actually be insolvent.

When the giant Lehman Brothers bank went down and the Federal Reserve refused to save it, shock waves went round the world. It was a seismic event in that cloistered world of banking which everywhere shut down on lending. It sent the system into a tail spin. Thus we became familiar with a new term: the credit crunch.

Returning to Greece, the bailiffs of the big boys, (the Troika’s IMF, ECB (European Central Bank) and the European Commission) have effectively moved in. Proud, humiliated Greece is being told it must provide collateral for the monies advanced. It must sell off all it can of its public sector along with whatever else can raise hard cash. The next thing we’ll be hearing is that they’ve slapped a ‘For Sale’ notice on the Parthenon. What has been needed throughout, but which has been totally lacking, is a generosity of spirit. If the 520 million people of Europe cannot handle 11 million, admittedly errant, citizens, then something is seriously wrong.

The fact is it is perfectly possible to be a member of the European family (i.e. the EU) – after all, there are nine of us who are not using the euro – without being beholden and tied to that flawed currency. It is equally possible that if one day that currency proves itself by correcting its inbuilt defects and then goes on to become the world’s reserve currency, replacing the dollar, we may ourselves rethink our position and apply to join. But that day is a long way off.

Meantime what of Greece and its mountain of unrepayable debt? 92% of the monies advanced to Greece do not go to helping that country get back on its feet, but to servicing its debts. As a deadline for repayment looms, Greece is handed monies which it must immediately pay back. Thus, while for book-keeping purposes, the situation seems under control it is anything but. It is an altogether hopeless situation. In essence it’s no different from that of a person taking up ever more credit cards to pay off a loan from his bank.

Europe, and in particular Germany, should remember that when the Americans put together that incredibly generous Marshall Aid programme to rescue them from an even more dire situation than present day Greece’s at the end of World War II, there was a total forgiveness of debt. Without that there would have been no recovery of Europe for decades. It remains my hope where little Greece is concerned that our great continent will show a generosity of spirit similar to what the Americans showed with their Marshall Aid programme and declare a forgiveness of debt. Without it Greece has no hope.

A tragic consequence of the present situation which few have thought about is that we are in danger of losing, through neglect and vandalism, much of that peerless heritage we so like to visit and wonder at. The treasures of European antiquity, of which the Greeks are custodians, are already suffering terribly from thefts and shocking neglect. What with the destruction going on in Aleppo, the oldest inhabited city on earth, at Palmyra, Babylon and indeed throughout the Middle East – the very cradle of civilisation – the world will wake up one day and realise that it wasn’t just present day humans who paid the price, but the surviving evidence of what its distant ancestors achieved down the ages.

The latter day Greek tragedy continues

If the Greeks vote no, they face not just potential mayhem but a complete national shutdown. Yet the majority of economists actually believe this course would serve the country best.

What are we to make of the tragedy which is unfolding across the beautiful waters of the Aegean? Here in high summer when they should be enjoying the fruits of their glorious holiday season they are locked in a battle for their very survival with the giants of north Europe and their banking systems.

Let’s be clear about one thing: Greece has already paid a terrible price for its profligacy and easy living on the back of a strong currency of which it was never qualified to be part. Their economy has had been bludgeoned by the money men into shrinking by a horrendous 25% and their youth unemployment exceeds 60%.

Right at the beginning, the books appealing for entry into the euro were cooked, helped in no small part by that ‘Great Vampire Squid’, Goldman Sachs. But while the Germans and the rest knew very well how the Greeks went about their business and that they were not a suitable candidate, political Europe had to take precedence over economic Europe and they let them in.

With other weaker economies such those of the Spanish, Portuguese, Irish and Italians allowed to join the party, the Germans ended up with a currency much less strong than their old Deutschmark would have been and that made it much easier for them to flog their BMWs and the like. Borrowing rates for these weaker economies became much lower than ever they would have been had they been using their own currencies so, of course, they were happy to buy north Europe’s products as well as treat themselves to a much higher standard of living than their economic performances warranted.

All was well throughout the goods times that preceded the financial crash of 2008. That ill-conceived monetary union – which lacked the also essential fiscal union – of the euro could bumble along so long as there were no headwinds. But, boy, it wasn’t so much headwinds that arrived but rather a hurricane. The Credit Crunch brought the Western world’s economies to the brink of meltdown.

Today the weakest of the dominoes stands in imminent danger of falling, with the risk that others will follow. And the country that benefited most during the good times, Germany, insists on playing hardball. It needs to show a bit of humility – as well as compassion – and realise that it must take its share of the blame for the plight that Greece finds itself in today.

Despite its own banks, along with French and others, being exposed to a possible Greek default of alarming proportions, it knows that a Greek economy that cannot grow because of acute austerity will never ever be able to pay off its debts. It needs relief and restructuring. Long before this present crisis broke they acknowledged this fact. But what now are the Troika’s proposals? Even deeper austerity. Can we be surprised that a government that was elected on a mandate to end austerity has thrown up its hands and said enough?

If Greece on Sunday, in its touching desire to remain at the heart of the European family – but also out of sheer terror at the thought of the consequences of being cast adrift – votes to accept the Troika’s diktats, it faces never-ending recession. If the Greek people vote no on Sunday, they will stay in the EU and possibly even the single currency, but mayhem could follow with a complete national shutdown. Could Brussels stand by and see this happen?

Actually the majority of economists believe that this seemingly bonkers course would serve it best (Argentina went down a similar road). Economists say there would be six months of hell, or possibly longer, but then a future would open up for Greece. With holiday costs cut to half their present level, we would cast aside that old warning to ‘beware of Greeks bearing gifts’. Greece would become the continent’s playground as never before. Poor, suffering Hellas, the first of all Europe’s civilisations, would start to smile again.

The house shortage conspiracy

The chancellor talks about helping people get on the housing ladder, but other than helping them get into more debt he has done very little. He knows which side his bread is buttered.

Conspiracies abound and conspiracy theorists make a good living pandering to our natural suspicions. The vast majority, including those surrounding Marilyn’s and Diana’s deaths, are nonsense. They persist because we find it hard to accept that famous people are subject to the same chance, and often malign, forces as the rest of us.

But that there are out there a fair few I have no doubt. I believe them to be almost a part of the human condition – from the tiny trader, like myself, who might wish for a private arrangement with a fellow trader not to undercut each other to a mighty conglomerate who might wish to do the same. OPEC is a perfect example. It has also to be accepted that the great majority are successful and that, as a result, we never get to hear about them.

I am a natural born sceptic – which perhaps has something to do with being called Thomas – and while I try to maintain an open mind, I have to admit that some theories are outlandish to the point of being funny. A couple which immediately spring to mind are that the pyramids were built by aliens and that the photos of the moon landings were trick photography.

I do, however, believe that the universe is teeming with ETs. With 100,000 galaxies in this universe – and science is starting to believe that there may be many universes – it surely is down to numbers. However rare may be the incidence of all the important factors coming together to make life possible – the so-called Goldilocks Effect – I find it inconceivable, with such numbers, that it only happened once. Furthermore, I believe that when these factors do coalesce, sooner or later, life is the inevitable consequence.

But returning to Earth and our penchant for conspiracies, I believe I have cottoned on to one which may go a long way to explaining why, when there is a clear need for many more houses, it never seems to happen. It is because the politicos are terrified of bringing about a downward spiral in the value of houses. It is not a conspiracy in which a handful of people have got together, but rather an acknowledgement that one’s home is typically his only significant asset.

Meantime, millions languish in rented, overcrowded and often substandard accommodation, desperate to buy their own homes but unable to do so because house price inflation has advanced at three times the rate of general inflation and as a result the deposit required is beyond their reach.

No one can argue against our desperate need to build more houses. Unlike Japan with fewer divorces, a falling birth rate and zero immigration, we are high on all three; people splitting from their partners need separate homes, a rising birth rate requires more houses (down the line), and millions moving to your country will require places to live.

During the recession the construction industry was the hardest hit. Didn’t it strike you as odd that its legions of unemployed were not put to work building this extra accommodation? The 100k houses built last year was less than half of what was required. What would happen if supply at long last rose to meet demand? The iron law of economics says prices would fall. What pushed house prices up to their present level, racing ahead of general inflation at a crazy rate? Easy credit and too many would-be buyers chasing too few houses. The real question is: if all the political parties are agreed on the need for more houses, why doesn’t it happen? After all, builders would set-to with a gusto and buyers would have not just a house but one at a more affordable rate.

Cameron and Osborne promised a relaxation of planning laws in 2010 and pledged to free up more land for development, but this government has so far failed miserably to deliver. Why is this? The answer, I fear, is that present mortgage holders have an interest in not just maintaining prices but contriving to force them up still further. They love a situation in which they are getting richer by doing nothing. Many are making more on their house annually than they are getting paid, with the difference being that living eats into their salary while nothing eats into their unearned capital gains. So just let a politician come along who threatens this nice little arrangement. That greatest of all feel-good factors would disappear down the plughole. To prick that love affair with rising wealth would make them incandescent with rage.

But in many ways crazy house prices might be compared to fools’ gold. Unless you’re going to flee abroad to a cheaper domicile or downsize, which most don’t want to do, then there are no tangible benefits. So how do the politicos keep them happy in this delusional state and excuse themselves from doing their duty to the homeless? First they acquiesce in keeping planning laws fiendishly difficult and listening too much to the ‘not in my back yard’ arguments. Then they waffle on ad nauseam about converting brown field sites. Then they pedal the greatest fiction of all: that our island is in danger of being concreted over.

Next time you fly over our green and pleasant land, look down and see what proportion of our lovely acres remain green. The Office for National Statistics have produced some very interesting figures on this. I invite you to read a BBC News article titled ‘The great myth of urban Britain‘. You will be happily stunned by the stats provided. It turns out only 2.27% of England’s landscape is built on. Just look out of your airplane window if you’re in any doubt.

Ensuring a sustainable economic recovery

Are we really out of the mess we got ourselves into six years ago? Can it be true that we are the fastest growing economy in the developed world? It would seem so, according to the statistics. But how are we achieving this? It is certainly not coming from the manufacturing sector, an area which Mrs Thatcher as well as her successors neglected in favour of the keep-your-hands-clean service economy. It’s coming from two quarters. First is an increase in investment from business.

At the height of the recession, when there was no money for anything, medium and large businesses were sitting on £75 billion of liquidity – twice the defence budget – which in the right climate they were ready to release. That climate, which is principally one of confidence, has finally come. The second factor which was depressing the whole of the economy was a moribund housing market. When houses start moving again it has a tremendous knock-on effect right across the board. Tired old carpets are thrown out; new kitchens and bathrooms installed; more stylish furniture acquired; dodgy roofs repaired; gardens landscaped and solar panels ordered; double glazing resumed; painting and decorating starts; the DIY stores hum; the list goes on and on.

But important as houses are, we mustn’t obsess about them. There are other things – like the ones which would earn us shed loads of foreign exchange, i.e. manufactured items. We were once so good at manufacturing and can be again. But if there is one area where there is huge room for improvement it is productivity: it is our Achilles’ heel. Why we are so sluggish here beats me. If we can get this up this summer of rejoicing – weather-wise and economy-wise – may open the sluice gates and propel us into a new era of prosperity.

That high risk policy of quantitative easing – essentially printing money – appears to have worked for us, but it didn’t work for the Japanese. They left it too late to begin and as a result entered what has been called the ‘lost decade’ of the nineties. In fact it has been more like two lost decades. They’ve never recovered their old elan. Our own emergency package to survive the financial crisis was more deftly handled, first by Mervyn King (though he was somewhat late dropping interests rates) and then by Mark Carney, both governors of the Bank of England. Perhaps our success has been part due to the City of London’s historic financial expertise

But alongside this, and despite their other cataclysmic failings, we must give credit to Gordon Brown and his chancellor, Alastair Darling. Once they realised the enormity of the crisis – on the Monday following that dire weekend when it struck and the ATMs would have dried up – they moved quickly and decisively to recapitalise the banks. As Wellington said after Waterloo: ‘It was the closest run thing you ever saw in your life’.

Brown’s successor in Downing Street was on a steep learning curve after his chancellor’s earlier silly mantra of ‘sharing the proceeds of growth’, and when he eventually wised up the results were there for all to see. But interest rates cannot stay as they are – it is so unjust to the prudent saver who for years has been bailing out the feckless spender. They must rise, and soon. When it comes it must be small and incremental, like a quarter of a per cent every couple of months; a policy of slowly, slowly catchy monkey, so to speak. This will help cool the overheating housing market.

We don’t have to worry too much about irresponsible lending as in the past, leading to wholesale repossessions, because the criteria today to get a loan and the deposit required has been massively tightened. Some complain that the hoops you have to jump through are as many as to adopt a child.

But two things, above all, are needed to sustain the recovery: first, a massive house-building programme to meet the demand that years of unrestricted immigration have imposed. This, too, will cool house price inflation and re-balancing our economy by boosting manufacturing; and second, markets should then be found for those goods beyond the still Doldrums-plagued Euro area. The obvious target ought to be that vast zone of good will to us, the former empire. With our shared history, common institutions and legals systems and, of course, language, it is calculated that we have a 21% financial advantage over our competitors.

It’s time to home in on a recovery

Are we seeing the first signs of confidence returning? We must earnestly hope so. Even that prophet of doom, Sir Mervyn King – the newly retired Governor of the Bank of England – is getting excited.

Our housing stock has greatly to be increased.

Houses prices, which never quite went into the tailspin of the US, are starting to rise again and mortgages are increasing. On balance, I think it was right to kick-start the badly hit building industry by government underwriting of mortgages. But this must be of limited duration. The last thing we need is for another bubble to start inflating. Hopefully the painful lessons of what happened before will act as a cautionary tale.

The fact is that our housing stock has greatly to be increased. The reason why house prices grew to such levels was that a fundamentally sound economic model of price determination was broken: supply was hugely below demand. And when that is put into reverse, the opposite price movement will happen: prices will fall. Last year we built 100,000 new houses, when most experts said it should have been 250,000. And it should have been at this level for years.

Those millions of immigrants that Tony Blair ‘sent out his search parties’ for have to live somewhere, as do the increasing number of people needing to be separately housed due to divorce and other factors. The point to remember is that when you build a house, you not only put builders, plumbers and electricians back to work but you create orders for carpets, furnishings, double glazing, electrical goods, furniture and much else besides. The knock-on effect is tremendous. Big infrastructure projects are all very well, but they are few in number, take years to process and are localised anyway. Huge swathes of the country see no obvious activity and don’t much benefit – if at all. But houses popping up from Lands End to John O’Groats do get noticed.

People’s income has been squeezed these past five years almost like never before. They have been subject to pay freezes, cuts, short time working and even lay-offs. And throughout all this time, the relentless march of inflation has eroded their disposable income. Even their taxes were going up. And while all this was going on, people desperately sought to pay down their horrendous debt levels. No wonder confidence went out the window and they felt unable to spend. When they looked around the world, the picture was just as grim – and in some cases much worse. Fear begets retrenchment and that, until this moment, is where we have been.

But now, with the stock market reaching its highest level since the turn of the century, banks being brought under control and being required to rebuilt their balance sheets (albeit at the expense of lending), medium and large size companies sitting on £70 billion and ready to go, houses shifting, mortgages easier to get and hundreds of thousands of new jobs being created, things are changing. Those straining-at-the-bit companies will feel encouraged to invest. Now the final – and critical – part of the jigsaw to be put in place is for people to get out there and start spending. And if they start to feel that the worst is over, they will. The rest will take care of itself. People, after all, do like to spend.

We have learned one hell of a lesson these past five years, and hopefully both government and people will act more responsibly next time round. But some real good will have come out of it all – as it always does: we are emerging leaner and meaner. The recession has forced us to address issues which we all knew had to be addressed, but which, while the good times rolled, we found excuses for putting off. We, individually, have been forced to examine every item of our domestic expenditure – but so too has the public sector. Now, at last, we are cutting away the fat which we allowed to accumulate in the public sector and, boy, was there a lot of it. Everything has to be justified. Any firm will tell you that, if it had to, in order to survive it could effect colossal savings. I, myself, have seen my shop takings drop by 25%, but I am still here. I cannot take much more, but my customers have not suffered. If anything, they are getting a better deal than ever and I am doing my level best to be even sweeter to them. But when central and local government were asked to do the same thing – very belatedly I might add – they squealed like stuffed pigs. And they had vastly more fat on them in the first place.

But, as they say, it’s an ill wind that blows no good. Soon, hopefully, we will have schoolchildren entering the job market with an education which can compare favourably with those hungry tigers in the East which are seeking to steal our thunder. Also we will have a workforce that knows and appreciates the necessity of becoming more competitive. Exports have already shown strong signs of picking up – although this has been mostly due to a weakened pound rather than anything else. Maybe, too, we will have put an effective break on those vast numbers of unskilled workers flooding into our little country who have put, unwittingly, such a strain on all our services. Even the NHS reforms may start to deliver, for as much as we love it, it cannot stay forever a holy cow which cannot be touched. We spend, now, as much as the European average, but we have nowhere like their standard of care. Where did all those scores of billions disappear? We doubled its budget in real terms in a decade. Perhaps it will improve now that it is to be under new management and not under the baleful control of that unrepentant apparatchik who presided over those scandalous deaths in North Staffordshire and who knows where else. And, finally, there is that lumbering giant, the Welfare State, who so many took for a ride. That, too, is being brought under control. Perhaps now we can get back to helping the genuinely needy, even alleviating their suffering more than we have previously been able. That would be good. So we do, very much, have positive things on the horizon. We must hope now that the Germans will continue to hold the eurozone together and stop the continent from imploding. That will give us even greater reasons to be hopeful.

We are busily re-orientating our services and export drive toward the still booming East – something which we should have done years ago. Even formerly-basket-case Africa is on a powerful upward trajectory. Uncle Sam, too, is showing distinct promise and is growing again at a healthy 2% with rising employment. He does, however, have some big problems which he has not addressed and only gets away with it, for the moment, because he stewards the world’s reserve currency – as we once did for so very, very long.

But, for our part, we must continue to hold our nerve with our own reforms. Only the police, it seems to me, remain a loose cannon among the great institutions of state. Though they have had cuts forced upon them, like almost everybody else, they still behave as though they a law unto themselves. More about that later.

We must get our railways back on track

We had better all pray that it will neither be a wet nor cold winter. That’s asking rather a lot seeing as it is the perverse British climate we’re talking about.

The reason for not being wet is that the water table from being alarmingly low at the start of the summer is now alarmingly high. Just a small amount of the liquid stuff and it will have nowhere to go except lie on the surface. Floods will then be inevitable and widespread, perhaps more than we have known in living memory.

As for not being too cold that is because we are a million miles from having repaired the pothole damage of the recent severe winters. To make matters worse the cost of keeping warm is going to be more than many people can bear, especially the old. We have had enormous hikes in energy bills – twice the level of general inflation.

This leads me to question of whether the wholesale privatisation of the utilities was a wise thing to do, especially where we have allowed so many of them to fall into foreign hands.

Apart from strategic aspects which we should always have an eye to, foreign companies care little if the British play up over being ripped off and obliged to pay more than the same company is charging in their own country. Naturally these companies are more sensitive to home criticism and will seek to minimise it there. The foreigner is seen as fair game.

Part of the problem is that there are only six or so major players – a similar number to the banks – and there is not genuine competition. Without a doubt real competition makes for efficiency and puts a brake on exploitative charges. It was right, as a consequence, to divest the taxpayer of as many of the lame-duck industries as possible – provided genuine competition could be introduced. I well remember how it was normal to wait for up to six weeks for a phone to be put in.

However, if we are sensible, we must accept that certain industries – and water is a good example – do not lend themselves to competition. Governments of all hues have known this, but were all so rapacious in getting their hands on the massive sums which the utilities could generate that they have been willing to sacrifice the national interest to do so.

And why, apart from common greed at the thought of all this lovely lolly, were they so anxious to do this? First, they had been so monumentally inept at balancing the national books that an infusion on this scale would camouflage their hopelessness; and second, they each had their own pet projects – mostly social engineering – which they were mad-keen to indulge.

Such indiscriminate privatisation as took place was not in the national interest. What was needed was an open-minded, selective approach and not one driven by short-term economic advantage nor an ideological zeal such as ‘privatise the lot’ or ‘nationalise all the commanding heights of industry’.

One very sad aspect of what has taken place is that the industry which this country pioneered, and as a result changed the world forever – the railways – is now a national disgrace, even a joke (albeit one in very low taste).

I almost wept when the last carriage-making facility in Leeds lost out to the Germans and this great industry, in the land of its birth, died. How sad that is.

A person could urge the prime minister in all earnestness to wade in over the railways. He would earn more brownie points than all his silly PR stunts like ‘hug a hoodie’, husky driving and riding a bike to the Commons put together. A recent poll has shown that 70 per cent of the nation would like to take the railways back into public ownership. As things stand, our ticket prices are almost the highest in Europe – four time that of Slovenia and three times that of Spain and Italy. The pricing structure is a nightmare of Byzantium complexity and the overcrowding of passengers an utter disgrace. At the same time umpteen 1st Class carriages lie almost empty. Speaking of this term – 1st Class – is unfortunate in itself, especially in this still most class-ridden of societies. Far better it be called Premium Rate.

A person could urge the prime minister in all earnestness to wade in over the railways. He would earn more brownie points than all his silly PR stunts like ‘hug a hoodie’, husky driving and riding a bike to the Commons put together. A recent poll has shown that 70 per cent of the nation would like to take the railways back into public ownership. As things stand, our ticket prices are almost the highest in Europe – four time that of Slovenia and three times that of Spain and Italy. The pricing structure is a nightmare of Byzantium complexity and the overcrowding of passengers an utter disgrace. At the same time umpteen 1st Class carriages lie almost empty. Speaking of this term – 1st Class – is unfortunate in itself, especially in this still most class-ridden of societies. Far better it be called Premium Rate.

Communications are at the heart of any country’s success or failure. It was the railways which opened up the world. The American west was won more by the iron horse than by Wild Bill Hickok and the vast riches of the Russian east by the Trans-Siberian Railway. We absolutely must get our railways back on track.

A train crash in slow motion

The euro crisis rolls on like a train crash in slow motion.

The fact is, you cannot bend economics to your will. The forces which say you cannot do this are almost as immutable as the laws of gravity. Yet that is what the founding fathers of the euro set out to do.

They sought to bind nations with wildly disparate national traits, and equally disparate levels of competitiveness, into one whole. But they did it for political reasons not economic.

It might have worked if all involved had applied the original, sensible rules of entry and submitted their annual budgets to a Brussels power of veto, but they did not.

A monetary union not backed by a fiscal one is actually a no brainer. It cannot work. Even those American founding fathers of nearly 250 years ago understood this.

The success of the American union had a lot to do with the template drawn from a single gene pool with a single historical experience, put in place by the original thirteen colonies who decreed a single language for all.

Now ‘cruel necessity’ – as Cromwell is said to have described the decision to cut off the king’s head – is pushing Europe to cut off the head of the errant Greek state and force it back to the Drachma, Europe’s oldest currency. It is also going to force those who remain within the single currency to give up forever sole control of their countries’ spending policies.

Having done that, then you might at last have a system which actually worked. Within that system would undoubtedly develop a super strong currency with the potential to displace the dollar as the world’s reserve currency.

It all hangs on what the Greeks vote for at the forthcoming election. Despite all the serious pain they are going through a surprising number of them (over 70%) still want to stay in the euro. But, being the hot-headed Greeks that they are, they cannot help but wear their pain on their sleeves.

If this shows itself by a massive protest vote for the party which promises to bucket a lot of austerity promises – as seems likely – then Greece’s days as a euro member are numbered.

The young and inexperienced party leader in question has convinced himself that the Germans, right now, need Greece more than the Greeks need the Germans. The logic of his argument is that the loss of Greece will begin the unravelling of the euro and quite possibly the whole ‘European Project’. He will simply refuse to implement austerity and defy the Germans and north Europeans to do their worst. He’s convinced they will blink first. I fear he and his nation are in for a terrible shock.

It has to be said that no one has benefited more from the euro than the Germans.

If they have huge reserves of savings that is because for a decade they have been marketing their products in a hugely (for them) undervalued currency. Their former chancellor, Helmut Kohl, has admitted – albeit belatedly – that at the time the political elite dared not ask the German people if they would surrender their beloved deutschmark in favour of the new currency because they knew that they would get a big fat nein.

Yet if the euro were to break up, their deutschmark would be back again – only this time with a vengeance; it would become so expensive that few could afford to buy their products. Exports would plummet.

So yes, the Germans are terrified that a Greek exit will set off an unstoppable chain reaction causing the weaker southern economies to drop out, threatening to destroy the whole single currency. But the Germans are equally terrified at seeing their hard earned savings and pensions going down a bottomless ‘Club Med’ plughole and an endless future of propping up lame duck economies.

So now the previously unthinkable is being touted in Berlin and the other chancelleries of Europe: Greece can go if it will not comply with its undertakings. It will serve as a salutary lesson to other possible backsliders, say some. Provided they do not show similar defiance as Greece, then I believe that Fritz will give the European Central Bank the powers it needs to act as the lender of last resort like the American Federal Reserve or the Bank of England.

Both for narrow self-interest and deep psychological reasons Germany does not wish the European Project to fail, much less be blamed for its failure. It wants desperately to be seen as a good European and lay forever the ghosts of its troubled past. So my own belief is that Germany will do all in it power to hold the eurozone together.

IIf the markets go on to attack the other weaker economies once Greece has gone, who knows where it will all end. Even German savings may not be enough to save the euro, so big are the debts of Italy and Spain, the 7th and 9th largest economies in the world.

George Soros, the man who bet against Britain staying in the ERM in 1992 and won a billion pounds in the process, says the euro train has three months before it hits the buffers. While he is not always right, we should worry. He is 60% of the time.

It is my firm belief, however, that the euro, in one form or another, will survive. And as strange – even weird – as it may seem, given present circumstances, there are still many countries waiting in the wings to join such as Poland, the Baltic states, Czech, Slovakia, Slovenia and even perhaps Sweden and Denmark.

Had the original rules of entry been adhered to then none of the present PIIGS would have qualified to join in the first place and this nightmare would never have happened. For that, Germany must take its share of the blame; it does no good for it to get on its high horse over-much.

But a reformed euro, even if it has shed a whole swath of weaker members, may yet be something to behold. It’s been a long time in Europe since anyone has been able to boast of sound money. If it did not entail so great a loss of sovereignty, it might be a door that we ourselves might one day find ourselves greatly tempted to knock on.

Germany: hero of the hour?

It used to be said that when America sneezed, Europe caught a cold. Now it’s the other way round, except that Europe has done a great deal more than sneezed; it’s almost taken to its bed. The reason for this is that Europe today is, despite appearances – the world’s economic powerhouse. It has on the way to twice America’s population and accounts for well over 40% of the world’s trade. But it has mismanaged its affairs to the point where the markets have had enough.

We must not blame the markets; they are only a reflection of how the guardians of our pension funds and insurance companies view future prospects. It is their job to identify risk and so protect people’s savings. They do not worry about the Scandinavians, Swiss, Dutch, Germans, or even us (now that we are in the process of balancing our budget and bringing our deficit under control). What they look for are not fine words and good intent – welcome as they are – but action.

They have seen it from us, but they have not been getting it in any meaningful way from Europe. From bestriding the world like a colossus in the lifetime of people still alive (not many, admittedly), Europe has seen its position twice destroyed by the two German wars.

The European Project was designed to ensure that this never happened again. For 50 years, Europe has painstakingly climbed back on its feet. Its people realised that old style nationalism was not the way forward, and today it is a beacon of cooperation and prosperity admired around the world. But all this is now threatened. Ruin, recrimination and bad – if not spilt – blood faces the continent unless it acts fast and decisively

It is to Europe’s great good fortune that it has one economy big enough and strong enough to silence the markets. But the leaders of that economy must step up to the plate. While we all understand why Germany is so paranoiac about printing money, no extra notes are actually printed – it’s just an electronic exercise in today’s world. And that is the point.

Today’s world is very different from the financial circumstances which brought Hitler to power. First, we now know that beggar thy neighbour, protectionist policies are counterproductive. Second, we are a much more joined up, globalised world, with powerful computers assisting our fragile brain capacities. Third, there are the great institutions such as the World Bank, the IMF, the World Trade Organisation, G20, and many, many more which were not in place when Germany’s Weimar Republic wrestled with its horrendous problems. (Not the least of these were the foolish and ruinous Reparations imposed by the victorious Allies in the Versailles Treaty). So Germany can take a more relaxed view today.

While it is important to learn the lessons of history, it is equally important not to be spooked by them. Germany has an historic opportunity to save Europe which its previous militarism helped to destroy. Germany must realise that if its fears and parsimoniousness allow the Euro to collapse, it will be among the greatest losers; its export-dependent economy would reel under the weight of a super valued Deutschmark. Nobody would be able to afford its goods. And that’s another thing! Nobody has benefited more from the reasonably priced Euro than have the Germans.

Poor, benighted Greece, (along, I might add, with the rest of us) has indulged itself on German products and that’s part of the reason it owes so much. There’s an irony in there somewhere, surely. Another irony is that this crisis has ended a British foreign policy which has been central to it for 500 years – even propelling it into any number of pre-emptive wars – never to allow a continental power bloc to develop which would overshadow us.

When our Prime Minister and Chancellor of the Exchequer urge Germany forward into a fiscal union, of which we will not be part, they are doing just that: putting the final building blocks in place which will lead to a united Europe.

It is a measure of the extraordinary trust which has built up that they feel safe to do so. So Fritz now has his chance to be the hero of the hour. Let him look at the big picture and rise to the challenge. Europe will be forever in his debt (literally). The European Central Bank must be the vehicle of his largess. It must be beefed up to the point where it can act like the Federal Reserve or the Bank of England – the lender of last resort.

The consequence of Germany opening up the coffers on all its hard earned dosh will not be without benefit in other ways. Systems will be put in place to ensure that such a drama never happens again; the feckless will be compelled into good housekeeping; corruption will be rooted out; Spanish practices in the workplace will be curtailed and Europe will have the fiscal union which, but for the crisis, it would never have had.

South Europe, despite all these measures, will always need a little forbearance, much like the poorer regions of Britain. We northerners will have to accept that with all that heat you will never get the Club Med countries to beaver away quite like us. But if they are unable to implement the austerity requirements – and they should not be too draconian (remember Versailles) – then they should be let go.

One thing, though, is certain. Either we all do our best to all hang together or we will surely all hang separately.

Taming Brussels

For a brief moment we thought we had got on top of the financial woes of the Credit Crunch and our personal and governmental debts which put all our livelihoods at risk.

At incredible potential cost, we had recapitalised our banks and put them on a sound footing. And then we began the painful long haul task of bringing our deficit under firm control. So far so good; the markets were impressed. The heat was off Britain.

But then the markets turned their gaze on the warring Europeans and their troubled, ill conceived euro.

The sovereign debt levels of the periphery countries quite spooked them. A slanging match had developed between the thrifty north and the spendthrift south. The Germans, in particular, were furious at the feckless and economically illiterate way the south Europeans had behaved, and the talk was that they had had enough of the haemorrhaging of their hard earned dosh. The whole future of the euro – and with it the European Union – hung in the balance.

Greece was the domino likely to go down first and very likely to carry a string of others with them. It was never an easy country to govern, and lovely people though they are, one of their irredeemable failings is that they make almost a national sport of not paying their taxes.

Yet at the same time, because they were part of the wonderful European Union, they expected to enjoy all the social benefits of the conscientious taxpaying north. How do you square a circle like that? After all, the north only got all those benefits because it was willing to cough up.

Greece’s public sector is bloated to the extent that it makes our own flawed product look like a sleekly toned race horse. What’s more, it only turns up for work when it feels like it and its appalling levels of absenteeism pass with just the Greek equivalent of a Gallic shrug. Then, after a semi-detached life of half work they insist on retiring ten years before the rest of us. No wonder the boys in their lederhosen are hacked off.

Yet despite what he and his other diligent north European comrades feel, he will not get his pride and joy deutschmark back. The ruling elite will see to that! The political classes have invested too much political and other capital in the so called ‘European project’ to let it founder. But after terrible dithering and lack of leadership which has propelled them to the wire, they have drawn back from what they see as the abyss of a collapsed Europe.

They are now determined, at last, to get ahead of the curve. They are putting together a package of such breathtaking proportions – three trillion (or 3,000,000,000,000) euros, no less – that even the money markets will recognise that they are putting their money where their mouth is and back off.

Yet the package will need approval of all 17 members of the eurozone and all 27 members of the Union for treaty amendments. Part of the deal, I’m sure, is that the people who underwrite the deal – principally the Germans – will insist on a future level of fiscal rectitude which will make it nigh on impossible for such a situation to arise again. There will be an oversight of all 17 member states’ budgets with a majority power of veto.

It will be, effectively, the final part of the jigsaw towards a united Europe: for all intents and purposes a fiscal union, which along with the existing monitory union will finally give the European single currency credibility. Politically, it couldn’t have happened at the beginning or at any point along the way, but dire necessity has forced the issue. It’s an ill wind that blows no good. The new Europe will not be such a bad place to belong so long as all that nonsense of an interfering Brussels is dealt with.

This is a heaven sent opportunity which will not come again. And because they need our signature on the treaty, we can insist on repatriation of those matters we all know to be flawed, such as the Working Times Directive, border controls, fisheries protection, and even that horney old chestnut: the Common Agricultural Policy.

Way back when we were haggling over the Maarstricht Treaty, they came up with that amazing word “subsidiarity”. What ever happened to it? It was adopted by the Union and was specifically designed to constrain Brussels.

If we seize the moment, we can then settle down to becoming the good Europeans we were always willing to be, instead of the perpetual awkward squad.

The world of tomorrow is going to be one of the big battalions, and Europe is a very big battalion indeed; one more than capable of stopping itself being pushed around by a resurgent China or anyone else.

The Perfect Storm

It is alarming that the markets have given a thumbs down to the Obama/Congress deal. And now we hear that they are seriously doubtful of Italy’s ability to grow its way out of the enormous debt it holds.

What with Spain teetering on the brink, and Greece, Portugal and Ireland considered lost causes, we have what amounts to ‘the perfect storm’. Yet we British have retained the market’s confidence; our willingness to bite the bullet allows us to borrow at the same rate as the Germans. But sadly that won’t save us. We absolutely have to sell our goods and services to the New World as well as the old.

43% alone of our output goes to the European Union, and another huge chunk to North America. The US Republicans – led by the Tea Party – refuse to aid a deficit cutting programme by including tax increases, even though the Federal Government’s tax take is barely half the European average. What right-minded system in today’s world allows Western drivers to fill up at not much more than half of the EU average?

Alas, Americans (and to be fair we) have been living high on the hog for too long. We in the West – especially the Americans with their consumption-driven economy – have been sating ourselves on China’s cheap goods, fueling its mind-blowing year-on-year 10% growth at the expence of increasing their own competetiveness. Industries have gone down like ninepins and jobs exported; they have allowed China to get away with a grossly undervalued currency and not to conform to World Trade Organisation rules. Perhaps most alarming of all, China stands accused of commercial and military espionage on a industrial scale by hacking into the West’s computer systems. This amounts to war by other means. So either the US treats balancing its budget almost as though it were a wartime priority, or it can say goodbye to being the world’s leading economy. Hello, China. Hello, India.

We may have been sold the idea that somethings are too big to fail, but believe me: a whole nation can fail – even the US if it hasn’t the stomach to put its house in order. The wars in Afghanistan and Iraq have done for the United States what the Kaiser and Hitler wars did for us… nigh bankrupted it. The difference is that in our case it was a noble struggle that simply had to be faced; a militaristic Germany bent on world conquest was a cause worth sacrificing even the British Empire for.

As far as the Euro is concerned, no matter how many sticking plasters they try to put over the crisis, nothing can hide the fact that the patient neeeds surgery. Greece and the others – the so called PIIGS – can’t service the debts they already have and provide for growth. And how does it help to foist more loans on them and push their service charges even higher? It’s the economics of the madhouse. They must all be cut loose; free to set their interest rates at the appropriate level; free to make a mess of things if they can’t get their act together without dragging everyone else down with them and also free to rejoin if they get their house in order and meet the strict criteria of membership, which they were meant to meet in the first place but never did.

The only alternative is for the sound economies of the north to take fiscal control of the hopeless cases in the south. In other words, a Fiscal Union to add to the unworkable existing Monetary Union. In the long run the PIIGS would all be better off. But would they stand for it? Proud, broken Greece would find it exceedingly hard to take the teutonic medicine that Frankfurt would insist they swallow.

As for poor old Britain, we are left dangling in the wind, waiting on events over which we have no control, but which are certain to turn all our lives upside down. I would hazard a guess, however, that if the Euro is reformed so that only successful economies can belong, then perhaps a very good case could then be made for us to join

There are huge advantages to be had in belonging to a truly powerful currancy bloc that might well take over as the world’s Reserve Currency. I fear the dollar’s day may be done, but I wouldn’t underestimate Uncle Sam’s recuperative powers and his legendary can-do approach when fired up. But please, please don’t let the Reserve Currency be the Yuan if Uncle Sam can’t make it.

The euro

How could Greece’s economy, which makes up only 2% of the Eurozone, potentially bring the whole house of cards crashing down? It is down to what the jittery markets make of it all. If they believe that the new bailout’s austerity demands (the second tranche) are unenforceable on a people who are now close to ungovernable, then they will panic, and a panicking bond market cannot be resisted. Indeed, we British had firsthand experience of this on ‘Black Wednesday’. And besides, the Greeks don’t have the stomach for more austerity: they would rather default on their debts and tell north Europe to get stuffed; they see only a future of unending misery as things stand.

As for the still fragile and barely recovering banks, there would inevitably be huge shockwaves all over again. But it’s the thought of a domino eftect on the other tottering economies of south Europe (Britain in extremis will save Ireland from going under) which is the stuff of sleepless nights. No body (neither the ECB nor IMF) can raise the sort of money needed to save the likes of Spain or Italy: it is truly a doomsday scenario which, amazingly, has got even China and India thinking they might have to step in.

The Euro is going to have to go back to the format which it originally drafted; that’s to say that only economies which can meet the five strict criteria laid down can be members. Alas, it was the failure to adhere to these requirements and the mad rush to admit anybody and everybody – and all the fudging that took place besides – which has led to the present situation. In that sense, north Europe has only itself to blame for not insisting on admission rules being sacrosanct. It is perfectly understandable that the hardworking, tax-paying, late-retiring North resents the happy-go-lucky, tax-avoiding and lets-play-the-Euro-system-with-its-cheap-loans South, which told a string of porkies about its indebtedness and then, to cap it all, wants to put its feet up early. But the South did only what most would do in the circumstances, given half a chance. Any thinking person could have seen it coming.

Watch this space!